FHA Improve Refinance: The goals as well as how It truly does work

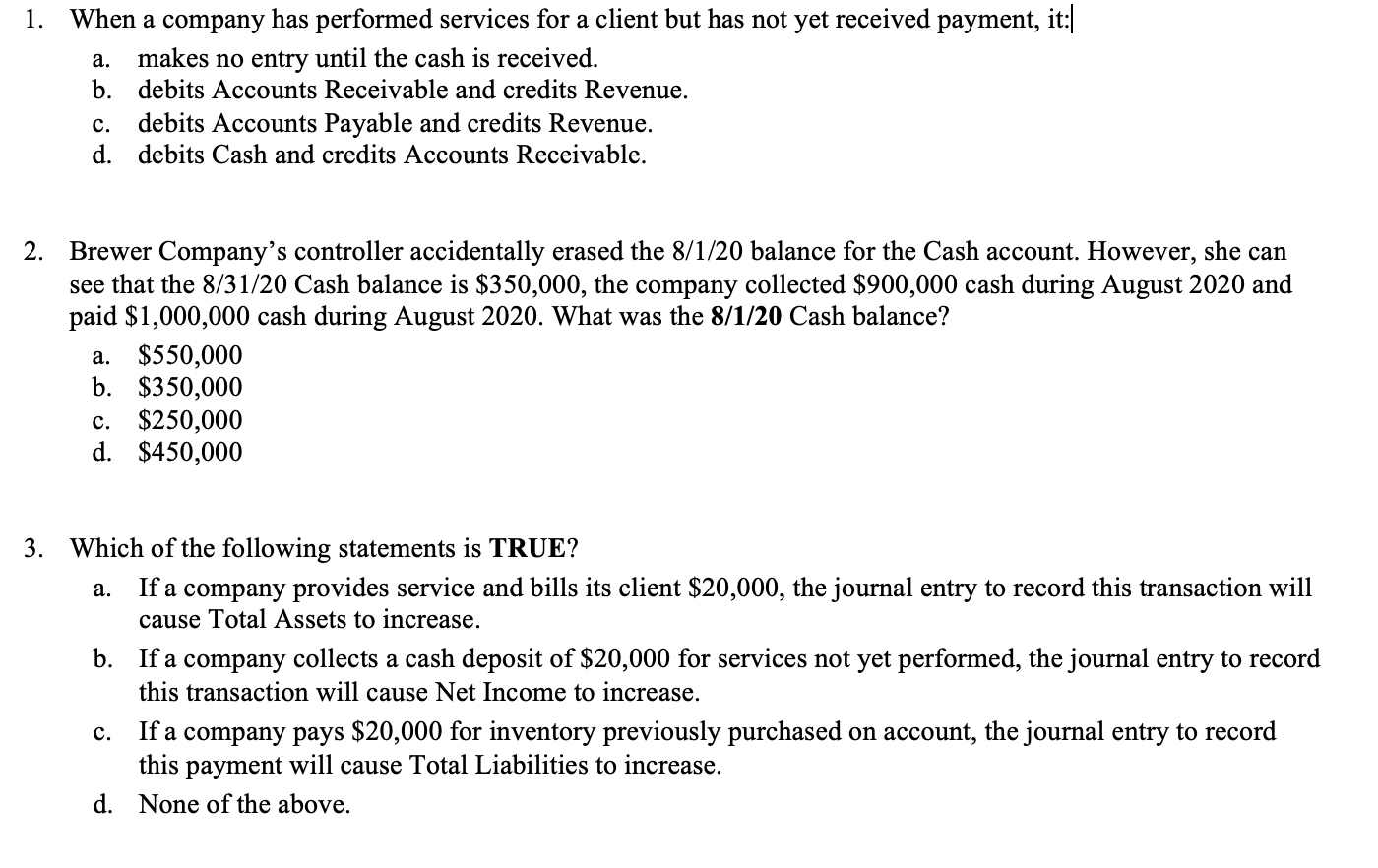

Selecting a faster, convenient answer to re-finance the FHA mortgage? An enthusiastic FHA Improve Re-finance will help. A keen FHA Improve Refinance also offers a faster, more affordable option for newest FHA borrowers seeking re-finance so you’re able to yet another FHA loan. That means quicker documents, a lot fewer costs, much less day waiting for underwriting to examine your loan software.

What’s a keen FHA Streamline Re-finance?

FHA Streamline Refinance try financing crafted by the fresh Government Property Administration to aid homeowners make their FHA mortgage inexpensive as opposed to the duty away from an extensive certification techniques. Convenient certification form an easier, much easier process to you, the newest citizen.

And, it’s a victory-earn on FHA. Because they already insure your own mortgage, they assume there is certainly a lowered chance that you’ll standard. Meanwhile, these are typically assisting you get a good, more affordable loan.

Which are the masters?

The FHA’s improve re-finance system contains a lot of positives for borrowers exactly who qualify. We have found a simple listing to offer an idea:

- Lower your price and/otherwise payment just like you manage with a conventional financial re-finance.

- Considering since the a good five-season varying-speed financial (ARM) otherwise since a predetermined-rate mortgage with a phrase away from 15, 20, twenty-five, otherwise thirty years.

- Straight down borrowing from the bank requirements.

- Limited files. This means zero earnings conditions, no proof employment, no paying up lender statements, and no investment verification requisite.

- Zero home security? No problem. Limitless LTV setting you might be nevertheless qualified even though you have little or no security of your home.

- No appraisal requisite.

How does an enthusiastic FHA Streamline really works?

Naturally, as with any money your borrow, specific constraints apply. For just one, there must be a confirmed net real benefit within the an excellent FHA Improve Re-finance transaction. Internet real work for setting you could only would an enthusiastic FHA Improve Refinance if it advantages you. Create a great FHA Improve Re-finance reduce your rate of interest? Wouldn’t it convert your current financial from an arm to help you good fixed-price loan? Put differently, would it not leave you within the a far greater updates than before? High! That’s the style of debtor the newest FHA is looking so you’re able to serve making use of their FHA Improve Re-finance program.

You simply can’t boost your mortgage equilibrium to cover refinancing will cost you and you can your brand-new financing cannot exceed the first mortgage number. Should you good FHA Streamline Re-finance, your brand-new loan amount is restricted to the current Jackson Lake loans no credit check prominent harmony as well as the upfront mortgage advanced. That means you are able to often need to pay settlement costs out-of wallet or rating an excellent no-cost financing. And really, no-cost is always to indeed feel titled no aside-of-wallet will set you back as it mode your own lender believes to spend the newest settlement costs for individuals who commit to spend a higher interest.

What are the cons?

In the event that bringing cash-out in your home collateral is the purpose, an FHA Streamline Refi may not be best for you. As to the reasons? Since you can’t have more than just $500 cash return for slight customizations to summarize costs.

Just like your totally new FHA mortgage, a keen FHA Improve Refinance nevertheless needs you to pay home loan insurance in both a-one-time, upfront home loan premium, that you pay in the closure, and you can a monthly home loan insurance policies commission.

How to be considered?

The financial need to be current (perhaps not delinquent) after you sign up for your FHA Streamline Re-finance. You are only allowed to build you to definitely late percentage on your newest FHA mortgage prior to now season. As well as on top of this, the mortgage repayments going back 6 months have to have already been made within 1 month of their due date. While the FHA Improve Refinances need quicker confirmation, this kind of payment record will teach your own lender as well as the FHA that you could responsibly pay off your current mortgage.

In the long run, you truly need to have made no less than half a dozen monthly payments towards the financial becoming refinanced, plus the half dozen latest payments need become produced towards the time. At exactly the same time, at least six months need introduced as first percentage owed. At the least 210 weeks have to have introduced once the go out your finalized.

The conclusion

It is essential to keep in mind about an enthusiastic FHA Streamline Re-finance is that you could only be eligible for so it loan when you are refinancing your current FHA financial to a different FHA home loan. When you’re refinancing so you’re able to or of a new loan sort of, this option is not readily available. Thankfully you to definitely since you already qualified for a keen FHA loan once you ordered your home, it’s nearly protected you’ll be able to be eligible for a separate FHA financing whenever you refinance.